- optimization

- probability

- neural networks

- machine learning

- differential equations

- pca

- financial analysis

- optimal stopping

- backward induction

- dynamic programming

- ergodicity

- utility theory

- decision theory

- a/b testing

- bootstrap

- concentration inequalities

- neural networks

- probability

- optimization

- finance

- data analysis

- mathematics

- computer science

- economics

- statistics

- data science

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

-

When t-Tests Fail in A/B Testing

Why standard t-tests break down with skewed data and how bootstrap methods and concentration inequalities provide reliable alternatives for A/B testing.

-

The St. Petersburg Paradox, Re-Run Over Time

How an old paradox reveals a deep flaw in classical economics and points the way to a more realistic model of human decision-making.

-

The Button Game: When Should You Stop for the Best Prize?

An interesting interview question about optimal stopping.

-

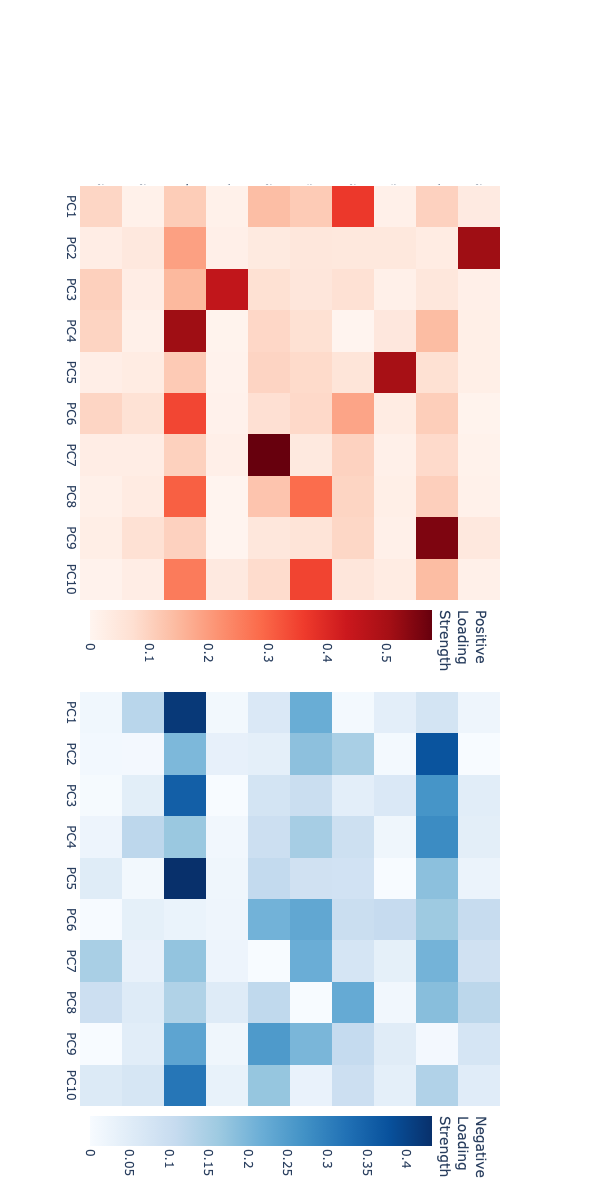

Detecting Regime Shifts in SP500 Stocks Using PCA and Sparse PCA

This project explores PCA and Sparse PCA on 457 SP500 stocks, using 2-minute interval data over 31 trading days (August 8 to September 19, 2024). The focus is on experimenting with dimensionality reduction techniques to identify regime shifts and key factors driving stock returns.

-

The Damped Unforced Pendulum Problem

Applying physics-informed neural networks to ODEs